Action Needed on the SAVE Plan

What SAVE Borrowers Need to Know Now: How the Plan Is Changing and What to Do Next

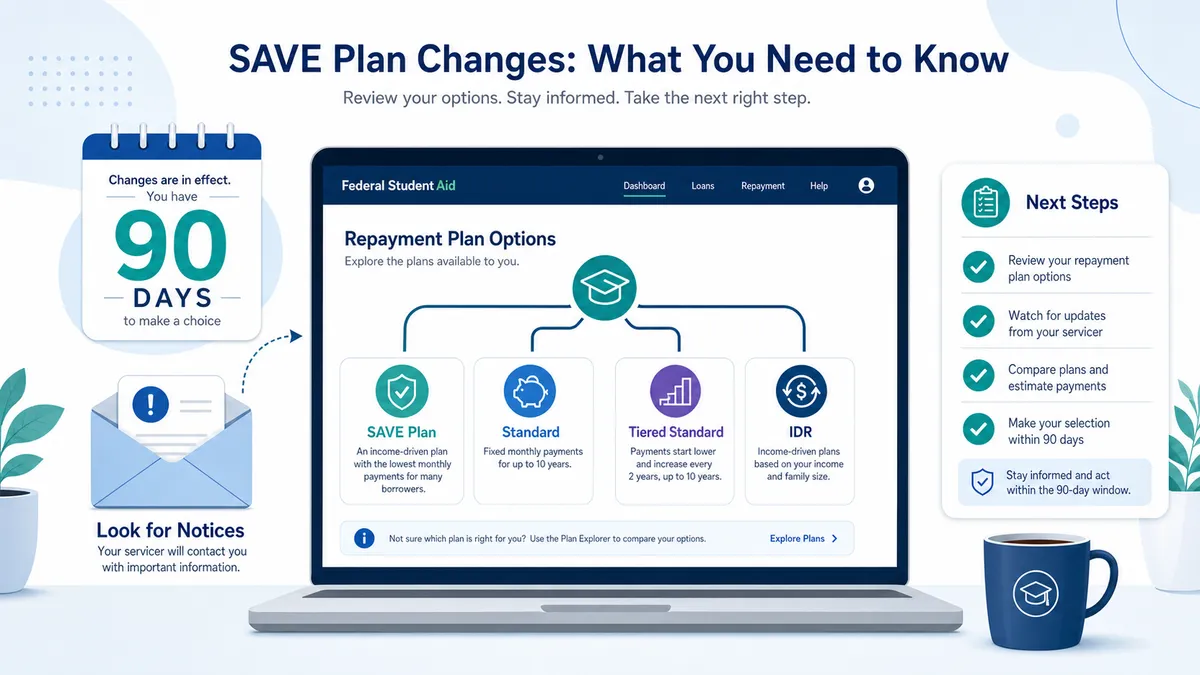

If you’re on the SAVE plan, the headline is straightforward: SAVE is ending, and borrowers will need to move into another repayment plan over the next two years. The most important next steps are to identify your loan servicer, log in, review your repayment options, and make a selection before your transition deadline passes.

What’s happening to the SAVE plan

The SAVE plan was designed to lower monthly payments for many federal student loan borrowers, but court rulings and subsequent policy changes have put it on a path to elimination. The Department of Education says it will stop new SAVE enrollments, deny pending SAVE applications, and transition all current SAVE borrowers into legal repayment plans.

Starting on July 1, 2026, federal loan servicers began issuing notices telling SAVE borrowers they must exit the plan and choose a new repayment option within at least 90 days. That deadline is tied to the date of the notice from your servicer, not just the calendar date, so borrowers need to watch their email, mail, and online account carefully.

Why this matters

For many borrowers, SAVE offered lower payments and more favorable terms than older plans. As it disappears, borrowers may face higher monthly payments, different forgiveness timelines, and new paperwork to move into another income-driven or standard repayment option.

That makes early action important. Logging in now gives you time to compare plans and avoid being defaulted into an option that may not fit your income or overall budget.

How to find your loan servicer

The easiest starting point is the official Federal Student Aid website. Log in with your FSA ID and go to My Aid to view your federal loans, your servicer’s name, and the contact information attached to each loan. If you’ve forgotten your FSA ID, you can recover it directly on studentaid.gov.

Once you know your servicer, visit its official website and log in or register for online access to review notices, repayment details, and plan selection options for your account. Common servicer sites include Nelnet, MOHELA, Aidvantage, and EdFinancial. You can also check your credit report to see who your servicer is for free at FreeCreditReport.com.

How to review and choose your options

After logging in to your servicer portal, look for sections labeled Repayment Options, Manage Repayment, or Change My Plan. That’s typically where you’ll see your current plan status and available replacement plans.

Before choosing, borrowers can compare projected payments using the Department of Education’s Loan Simulator. If you want an income-driven replacement plan, you can submit the official request at studentaid.gov/idr, which routes the application to your servicer for processing. For official updates about the SAVE litigation and transition process, borrowers should also review the Department’s IDR court actions page.

What happens if you miss the SAVE transition deadline

If you miss the deadline in your servicer notice, you won’t stay in SAVE. Borrowers who do not transition within the 90-day period communicated by their servicer will be automatically enrolled in either the Standard Repayment Plan or the new Tiered Standard Plan.

That matters because Standard and Tiered Standard plans usually set payments based on the loan balance and repayment schedule, not on your income, which can make the monthly bill much higher than what you were used to under SAVE. Missing the deadline does not necessarily lock you into that plan forever, but it can mean a higher payment right away and more scrambling later to request a better fit.

What to do now

A practical next-step checklist looks like this:

- Log in at studentaid.gov and confirm your servicer.

- Log in to your servicer’s website and read any SAVE-related notices or deadlines.

- Use the Loan Simulator to compare monthly payment options.

- Submit a request at studentaid.gov/idr if you want an income-driven replacement plan.

- Save copies of notices, confirmation emails, and any correspondence from your servicer.

Borrowers who act during their notice window will have more control over what comes next and a better chance of picking a plan that fits their income and other financial obligations before automatic reassignment happens.